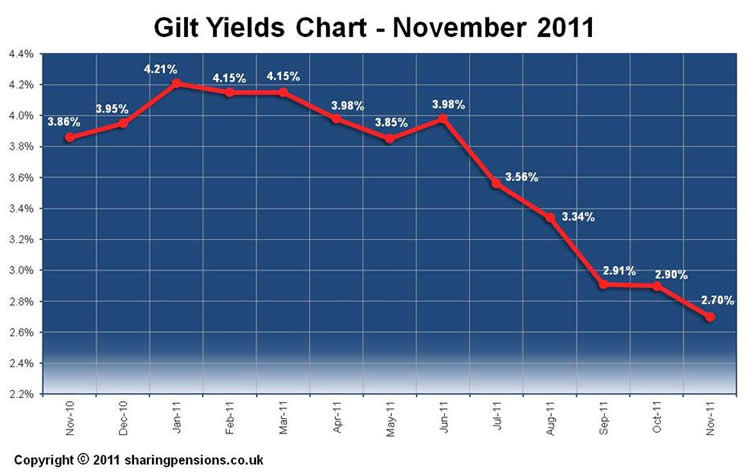

The 15-year gilt yields Fig 4 shows a significant reduction in the yields from 3.98% in 30 June 2011 to today with yields at 2.70%. This is due to the latest from the Eurozone with Greece to decide the agreed bailout in a referendum and the possibility this could lead to a Greece default.

Annuity rates are linked to gilt yields and as a rough guide a 25 basis point change in gilt yields translate to a 2.5% change in rates. Although providers may not change the rates immediately, however, eventually they will adjust rates to reflect the 15-year gilt yields. For the month of October the gilt yields finished down only 1 basis point but the standard annuity rates reduced by 0.40% or the equivalent to 4 basis points. For September annuity rates did not reduce as much as expected so with most annuity rates reducing by 0.25% to 1.5% in October we start November with annuities balancing out against gilt yields in the short term.

To the end of October 2011 the 15-year gilt yields had reduced by 108 basis points since 30 June 2011 and annuity rates by 10.48% so this is very similar. On the 1st November with gilt yields at 2.68% and 22 basis points down for the month already it suggests annuity rates across the board will fall 2.2% if gilt yields do not recover.

The FTSE-100 index had reduced from 6,000 by the end of June to 5,313 by the end of November and as money moves to buy gilts the price increased thereby reducing the yield. This shows a close link between the equity markets and the gilt yields as investments moved from equities to gilts with greater uncertainty in the future of Europe and global recession.

With both equities and annuity rates falling, this has resulted with a double negative impact on pensioner income where their pension funds reduced and the annuity based on this lower fund.

The decrease in the 15-year gilt yields for November 2011 have been due to the uncertainty over the Greek debt and the referendum announced by the Greece Prime Minister George Papandreou. Equity markets increased with the bailout plan agreed by the Eurozone with the FTSE-100 index closing at 5,713 on 27 October. Gilt yields also ended strongly for the week at 3.08% only to fall during early November to end the first week down 30 basis points at 2.78%. There is still uncertainty due to the political changes and the knock on effect with Italy's debt reaching unsustainable levels with the cost of their borrowing rising and this may further reduce pension annuity rates.

Fig 5 below shows the daily 15-year Gilt Yield and the increase or decrease from the previous day's close:

| 15-Year Gilt Yields - November 2011 |

| Mon 31st |

Tues 1st |

Wed 2nd |

Thurs 3rd |

Fri 4th |

| |

| 2.68% |

|

|

0.22 |

|

| 2.74% |

|

|

0.06 |

|

| 2.83% |

|

|

0.09 |

|

| 2.78% |

|

|

0.05 |

|

| Mon 7th |

Tues 8th |

Wed 9th |

Thurs 10th |

Fri 11th |

| 2.75% |

|

|

0.03 |

|

| 2.71% |

|

|

0.04 |

|

| 2.63% |

|

|

0.08 |

|

| 2.65% |

|

|

0.02 |

|

| 2.74% |

|

|

0.08 |

|

| Mon 14th |

Tues 15th |

Wed 16th |

Thus 17th |

Fri 18th |

| 2.65% |

|

|

0.09 |

|

| 2.58% |

|

|

0.07 |

|

| 2.60% |

|

|

0.02 |

|

| 2.66% |

|

|

0.06 |

|

| 2.70% |

|

|

0.04 |

|

| Mon 21st |

Tues 22nd |

Wed 23rd |

Thurs 24th |

Fri 25th |

| 2.66% |

|

|

0.04 |

|

| 2.63% |

|

|

0.03 |

|

| 2.59% |

|

|

0.04 |

|

| 2.60% |

|

|

0.01 |

|

| 2.72% |

|

|

0.12 |

|

| Mon 28th |

Tues 29th |

Wed 30th |

|

|

| 2.66% |

|

|

0.06 |

|

| 2.62% |

|

|

0.04 |

|

| 2.70% |

|

|

0.08 |

|

|

|

|

| |

Fig 5: Daily 15-year gilt yields and changes |

|

Fig 5 above shows gilt yields started November at 2.90% which is a reduction of 1 basis point from the start of October. This should translate to roughly a 0.1% reduction in annuity rates and providers have accounted for about 0.40% of this by 31 October 2011. This over reduction absorbs the shortfall from the month before to bring a balance between rates and gilts. Since then the 15-year gilt yields reduced on the first day by 22 basis points suggesting a 2.2% fall in annuity rates if the gilt yields do not improve.

|